Silicon Valley Bank is no more. The tech industry’s go-to lender imploded in the second-largest bank failure in US history. After investor concerns about Silicon Valley Bank’s (SVB) solvency prompted a bank run, the Federal Deposit Insurance Corporation (FDIC) took control of customers’ deposits yesterday.

The collapse happened fast:

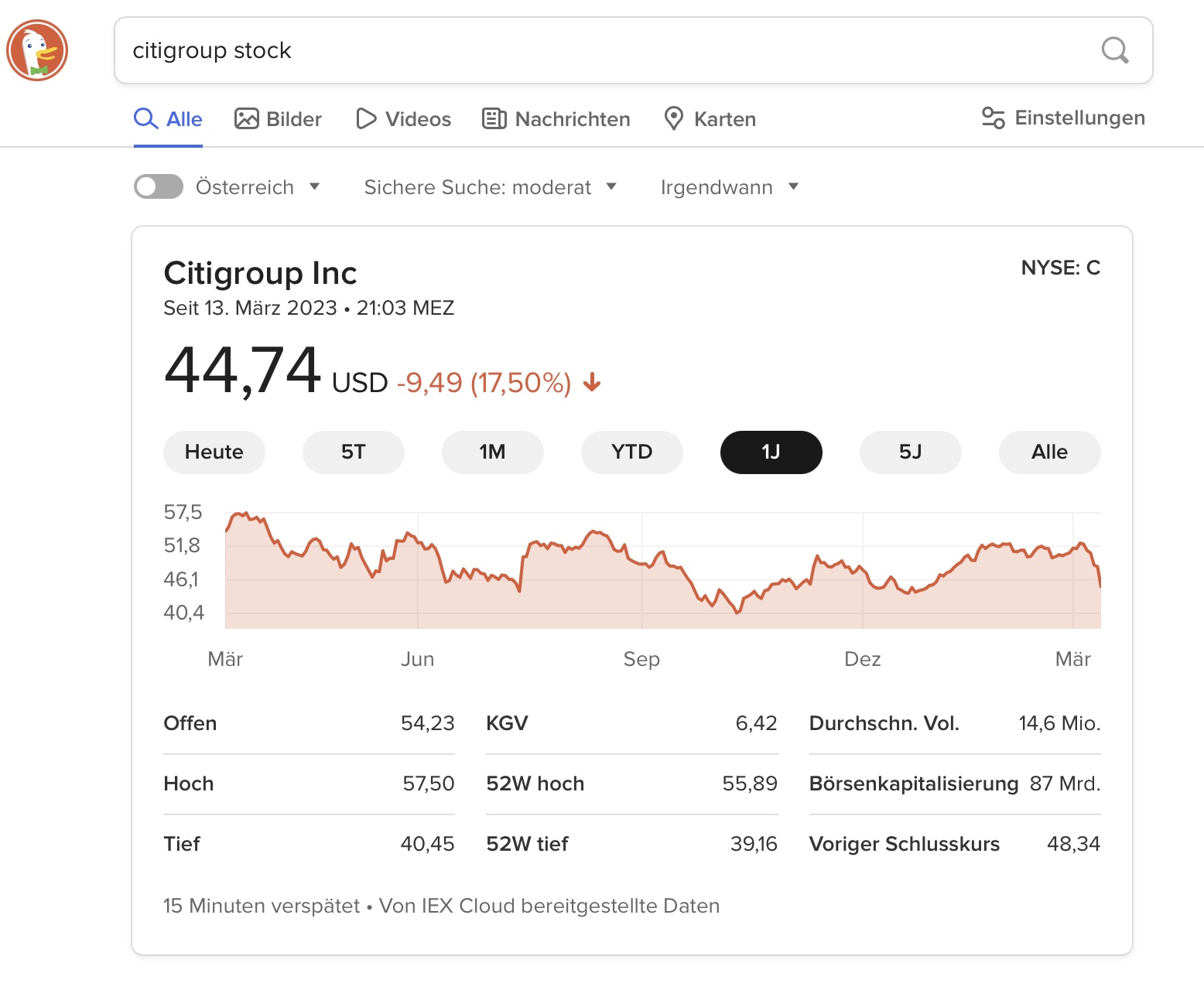

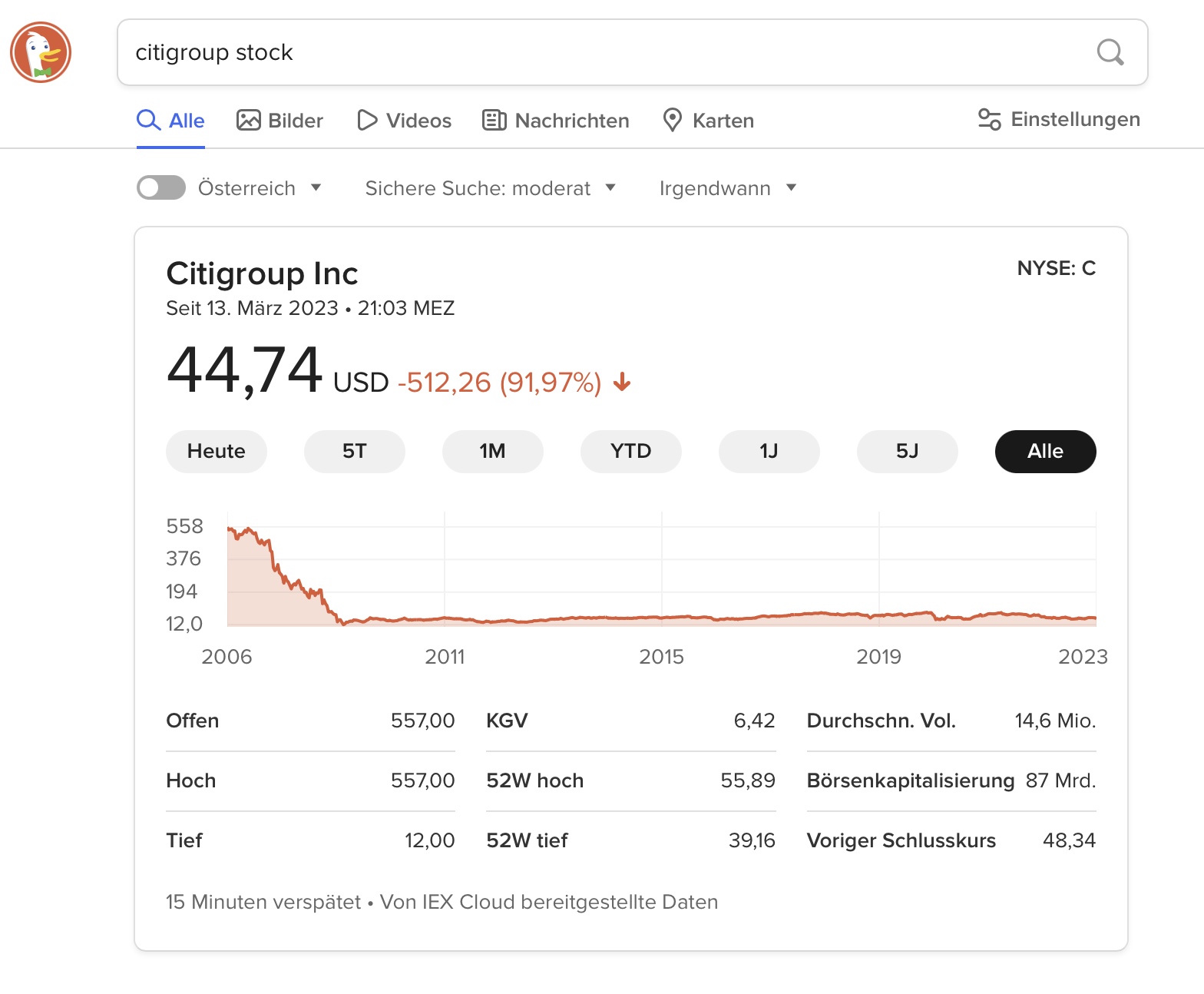

SVB said Wednesday that it sold some of its assets at an almost $2 billion loss, sending investors and depositors into full freak-out mode.

Its stock tanked over 60% the next day, and several prominent VC funds advised their portfolio companies to pull their deposits.

I put my money in a bank, then the bank loans it to someone else. I still think I have that money, but so does the person who gets a loan.

This seems a bit like a Ponzi scheme, but the system works great until something happens that causes a significant percentage of the bank’s customers to become concerned about the bank’s solvency. They rush to get their money out of the bank, but it doesn’t have enough cash in reserve to cover all the withdrawals, so the bank fails.

In the U.S., the FDIC steps in to take control of the bank and guarantees that all the bank customers will get their money, even if it means the federal government has to foot the bill. Again, this works great because it gives people confidence that, even if the bank fails, they’ll get their money.

When this happens to a bank or two at a time, it’s no big deal. What scares me is if the withdrawal panic begins spreading. People at other banks begin withdrawing their money to be safe, which causes others to panic and withdraw their money in an expanding downward spiral that turns into a national catastrophe where the federal government needs to invent trillions of dollars to pay off all the bank depositors in hundreds or thousands of banks. The stock market crashes and inflation skyrockets. The country dives into a deep depression that spreads around the world. It’s the 1930s all over again.

Yeah, it’s spooky when a big bank fails because, under the right circumstances, it could start the chain reaction I just spelled out.

Money for loans gets created out of “thin air”* in the moment when the bank books the money to your account at the same bank. This is called commercial bank money creation.

If this money leaves the bank for instance because you buy something and the seller uses a different bank your bank eventually has to compensate it with new deposits but only the part that didn’t come back on other ways for example by the loan created by another bank which floats to a seller at your bank and only at the end of the day or week.

Only a fraction of circulating money is issued by the Federal Reserve Bank System. The rest is electronically issued by commercial banks in form of loans.

In times of so called quantitative easing the part from the FED can be larger than usual.

Yeah, I already understood how it works. But I didn’t want to preface my post with a long lesson in macroeconomics, so I boiled it down. It’s also why I followed up with the statement that depositors still have their money, even though the bank subsequently lends a percentage of that money to borrowers who also think they have the money. So yes, you’re right; in effect, banks create money, which finances economic expansion. It’s also how governments finance deficits by creating money through the sale of marketable securities.

My bigger point is that it’s something of a house of cards that works quite well as long as people remain confident that it works and their money is safe. Ensuring that bank failures don’t cascade into a domino effect of bank runs that overwhelm the system and collapse the house of cards is the primary purpose of the FDIC (in the U.S.), which insures bank deposits and, when a bank fails, assumes control of the bank to recoup as much money as possible by liquidating the bank’s assets (mostly loans the bank made that are, as you pointed out, backed by collateral).

Yes. This time, unlike in 2008, that could be used as a reason to introduce Central Bank Digital Currency.

This would be both stabilizing and a great threat to all kinds of freedom.